Table of Contents

Straight-Line Depreciation – Definition

Straight-line depreciation is a method of uniformly depreciating a tangible asset over the period of its usability or until it reaches its salvage/scrap value.

Most businesses use this method of depreciation as it is easy and has comparatively fewer chances of errors. At the end of its useful life, the asset value is nil or equal to its residual value.

Depreciation is the decrease in value of a fixed asset due to wear and tear, the passage of time or change in technology.

In this method, you need to debit the same percentage of the asset’s cost each accounting year. It reflects a straight-line on the graph of asset value over its life span.

Hence, it is known as a straight-line or fixed percentage depreciation method.

How To Calculate Depreciation Using Straight-line Method?

When you purchase an asset at the beginning of the accounting year, you need to calculate the depreciation for a complete year.

It can be calculated in 2 ways:

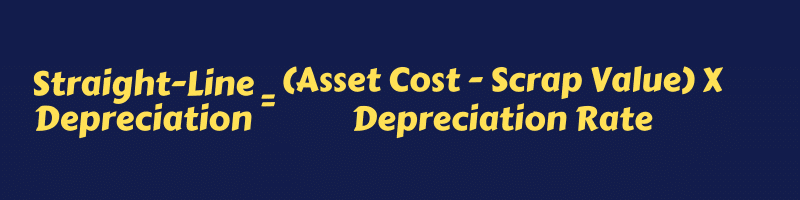

- Subtract the scrap value from asset cost and divide it by the number of years of its useful life.

- Subtract the scrap value from asset cost and multiply by the depreciation rate.

Formulas to Calculate Straight-line Depreciation

It is not always the case that a company purchases an asset at the beginning of the accounting year. Hence, you need to depreciate the asset partially for that year.

To calculate the depreciation for a partial year multiply the depreciation of full-year with the number of months and then divide it by 12.

Formula to Calculate Straight-line Depreciation Rate

To calculate the depreciation rate, divide the annual depreciation amount by the value left after deducting scrap value from the asset cost.

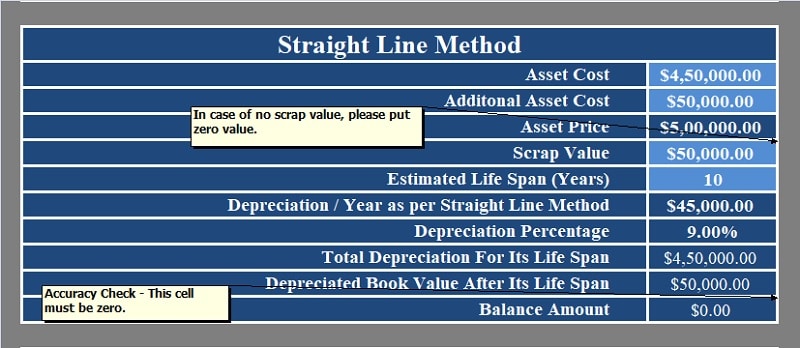

Example of Straight-line Method

Let us understand all the above-mentioned 3 formulas with an example.

Asset Value: $ 50,000

Estimated Useful Life: 10 years

Scrap Value: $ 5,000

Applying the above formula:

= ($ 50,000 – $ 5,000) / 10 Years

= $ 45,000 / 10 Years = $ 9,000 Per Year.

Applying Depreciation Rate:

= ($ 50,000 – $ 5,000) X 20%

= $ 45,000 X 20% = $ 9,000 Per Year.

In case the asset is purchased after 6 months of the beginning of the accounting year the partial depreciation will be calculated as follows:

= $ 9,000 X 6/12

= $ 4,500

Partial Depreciation for that accounting year will be $ 4,500.

Depreciation rate will be calculated as follows:

= $ 9,000 / ($ 50,000 – $ 5,000) X 100 = 20%.

You can also calculate straight-line depreciation using SLN Function in excel. You can also use a simple and easy Depreciation Calculator Excel Template with predefined formulas.

Accounting Entries of Straight-line Method

Given-below are he journal entries for straight-line depreciation

Journal Entries in Year of Purchase:

Asset A/c Dr

To Cash/Bank/Creditor A/c Cr

Depreciation Journal Entry:

Depreciation A/c Dr

To Asset A/c Cr

Income Statement:

Profit & Loss A/c Dr.

To Depreciation A/c. Cr

Eventually, the balance sheet will reflect the decreased value of the asset from the Asset A/c at the end of the year.

Advantages of the Straight-Line Method

- Simple Calculations

- The asset can be written off completely.

- Suitable for small businesses.

- Fewer chances of errors.

Disadvantages of the Straight-Line Method

- Repair cost increases in later years.

- This method doesn’t take the loss of efficiency into account.

- Functional or useful life cannot be accurately measured and hence the depreciation calculated is considered illogical in some cases.

- No provision for replacement of the asset.

We thank our readers for liking, sharing and following us on different social media platforms.

If you have any queries please share in the comment section below. We will be more than happy to assist you.

Leave a Reply