A registered supplier is eligible to claim the bad debts Output VAT adjustments according to the Article (64) of UAE VAT Law.

These bad debt Output VAT adjustments are subject to specific conditions. Let us discuss the adjustments of Bad Debts in detail.

What are Bad Debts?

Before we proceed to understand the Article (64) regarding the Bad Debts Output VAT Adjustments we must first understand what are bad debts.

When a registered supplier sells goods to another registered recipient, there are chances of Bad Debts. The registered supplier has already paid VAT at the time of supply.

If the recipient fails to make payments in part or full to the supplier, it turns as bad debts for the supplier.

As the VAT is paid by the registered supplier at the time of supply of goods or services, the Vat paid is a loss to the supplier if no or part payment is received.

Thus, to ease the burden of excess tax on businesses, there is a provision of bad debts output VAT adjustments in the VAT Law.

Article (64) – Adjustments of Bad Debts or Bad Debts Output VAT Adjustments

Article (64) states that:

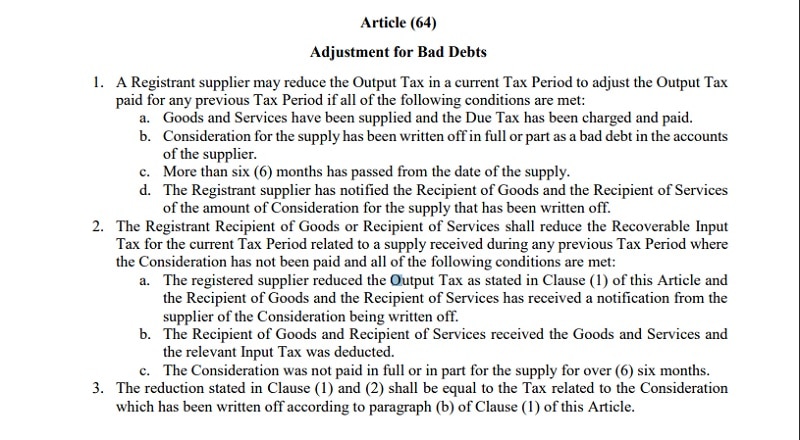

Clause 1

A Registrant supplier may reduce the Output Tax in a current Tax Period to adjust the Output Tax paid for any previous Tax Period if all of the following conditions are met:

a. Goods and Services have been supplied and the Due Tax has been charged and paid.

b. Consideration for the supply has been written off in full or part as a bad debt in the accounts of the supplier.

c. More than six (6) months has passed from the date of the supply.

d. The Registrant supplier has notified the Recipient of Goods and the Recipient of Services of the amount of Consideration for the supply that has been written off.

Clause 2

The Registrant Recipient of Goods or Recipient of Services shall reduce the Recoverable Input Tax for the current Tax Period related to a supply received during any previous Tax Period where the Consideration has not been paid and all of the following conditions are met:

a. The registered supplier reduced the Output Tax as stated in Clause (1) of this Article and the Recipient of Goods and the Recipient of Services has received a notification from the supplier of the Consideration being written off.

b. The Recipient of Goods and Recipient of Services received the Goods and Services and the relevant Input Tax was deducted.

c. The Consideration was not paid in full or in part for the supply for over (6) six months.

Clause 3

The reduction stated in Clause (1) and (2) shall be equal to the Tax related to the Consideration

which has been written off according to paragraph (b) of Clause (1) of this Article.

Click on the link below to download the UAE VAT Law:

Federal Decree-Law No. (8) of 2017 on Value Added Tax

You can download UAE centric VAT Templates like UAE VAT Invoice Template, UAE Invoice Template in Arabic, and Cash Book with VAT from our website.

Conclusions:

Article (64) Clause 1, 2 and 3 clearly defines that a registered supplier can reduce his output tax liability paid for any previous tax period if:

- VAT has already paid in full at the time of supply to FTA.

- The consideration of bad debts shall be fully or partly written off in books of accounts.

- Minimum of 6 months have passed from the date of supply of goods or services.

- The recipient has been duly informed of consideration of bad debts.

- A recipient has reduced his recoverable input tax for the tax period subject to the previously made supply of goods or services.

- The claimable amount will be subject tot he amount of Consideration written off.

- Documents will be required by FTA to support the claim.

This article is for educational purpose and should not be considered as legal tax advice. Consult local tax advisors for better understanding and implementation.

We thank our readers for liking, sharing and following us on different social media platforms.

If you have any queries please share in the comment section below. We will be more than happy to assist you.

Leave a Reply